The outbreak of war in the Middle East has upended some of the most popular trades of 2026 so far, catching global investors off guard in their widespread bets against the US dollar and in favour of stock markets outside America.

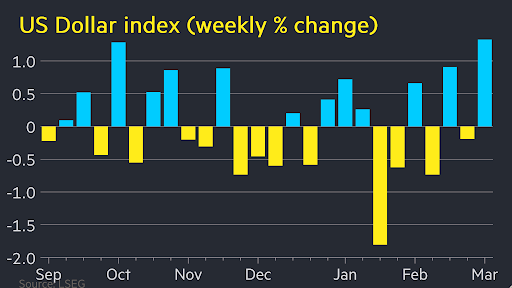

As investors have rushed to de-risk their portfolios in the face of soaring energy prices and fears of higher inflation, Wall Street indices have weathered the fallout much better than global peers, and the US dollar is on course for its best week in four months.

Meanwhile, previously buoyant Asian and European equities have suffered big losses and even gold — typically considered a safe harbour from inflation fears and geopolitical turmoil — has been swept up in the sell-off.

“There isn’t really anywhere to hide, everything is down, so it’s [a question of]: where are your exposures?” said Gerry Fowler, head of derivatives strategy at UBS. This is hurting “these really popular trades that have done well”, he said.

The US, which has become a net energy exporter since its shale oil revolution, is also considered to be less exposed to a price shock from the war compared with energy importers in Europe and much of Asia.

“The US will be in a better position to cushion any blow from sharply rising energy prices,” said Matthias Scheiber, head of the multi-asset team at Allspring Global Investments, while “Asia, Europe . . . they are all net energy importers”. Scheiber said he had reduced his exposure to Asian stocks this week because of rising energy prices.

The Stoxx Europe 600 has fallen more than 3 per cent this week, even after a rebound on Wednesday, while Wall Street’s S&P 500 is only marginally lower.

The selling has been more dramatic in east Asian economies. South Korea, the world’s eighth biggest oil importer and home to the world’s best-performing market of the year, saw its benchmark index plunge 12 per cent on Wednesday in a record one-day drop.

Alongside losses in markets dependent on oil imports, a broader “sell the winners” trade has taken hold in markets this week, with the sheer popularity of some non-US indices before this week contributing to the scale of the selling.

“The main thing that we have broadly seen in the recent sell-off is position squaring,” where investors with tight risk limits, such as hedge funds, sell assets that performed best recently, said Thys Louw, an emerging markets debt portfolio manager at Ninety One. “That is true whether it is Korean equities or the Egyptian pound.”

“Diversifying from US markets or being short the dollar was a main theme . . . you’ve had hedge funds or fast money getting out of a lot of these trades,” Louw said.

Global investors had been reducing their exposure to US assets in recent months, spooked by US President Donald Trump’s erratic foreign policymaking and fears about a bubble in the AI stocks that make up so much of the Wall Street benchmarks.

Investors had poured record sums into European equity funds in February, setting the region’s stocks up for a sharp fall when traders were forced to retrench.

Sharon Bell, senior equities strategist at Goldman Sachs, said that “a growing keenness to position into Europe has arguably made it vulnerable”.

Analysts said the move was exacerbated by the unwinding of leveraged positions, which had been gaining popularity with retail investors this year. Taiwanese and Japanese stocks, also popular bets at the start of the year, have tumbled this week too.

War in the Middle East: what’s the end game?

Join FT journalists on March 11, 1-2pm UK/GMT for our subscriber webinar. Register now and send us your questions.

Before the selling began, a months-long surge in equity prices in Europe, South Korea and Japan had seen the value of benchmark indices, compared with trailing earnings, reach their highest level since the Covid pandemic. That had pushed South Korea’s Kospi above 20 times earnings.

“What we’ve seen is basically a reversal of the trades that were working,” said Trevor Greetham, head of multi-asset investing at Royal London Asset Management, adding that the fund manager had been selling Japanese and emerging-market stocks in particular this week.

The dollar has also rallied as traders sought perceived havens, a stark reversal of investors’ bearishness towards the US currency before the conflict.

Lee Hardman, senior FX analyst at MUFG, said the de-risking was causing a “squeeze in crowded short dollar” positions; in other words, investors are being forced to ditch widespread negative dollar bets, which itself is sending the greenback higher.

The dollar has risen 1.3 per cent against a basket of the major US trading partners this week, while this year’s rallies in the euro and emerging-market currencies have rapidly unwound.

Kit Juckes, chief FX strategist at Société Générale, said he expects this week’s bounce in the dollar to last, even if the conflict is relatively shortlived. “We think the reset in major exchange rates will persist,” he said, because “the dollar index fell further [last year] than was justified by [relative interest] rate moves”.

How long the conflict lasts, and how much damage the region’s energy infrastructure sustains in that time, remains the key question for markets, say analysts.

Some investors expect the market to return to its bearish stance on the dollar once the worst of the conflict is over.

Luca Paolini, chief strategist at Pictet Asset Management, said he expects the dollar to act as a haven “in the chaotic phase of the market price action”, but added that, in the medium-term, this conflict will add to the “diversification away from the US impulse”.

Additional reporting by Ian Smith and Joseph Cotterill. Data visualisation by Ray Douglas